Last night on CNBC’s Fast Money, Marko Kolanovic, JPMorgan’s global head of derivative strategy made the case for an uptick in volatility, and the strong potential for a pullback in U.S. stocks nearing 5% between now and the end of the year:

Kolanovic’s expectation for a volatility pick up in the coming months has a lot to do with technical factors associated with hedging that suppressed volatility since the end of June, and obviously the upcoming presidential election. But in general is owes most to global central banks being far closer to normalizing monetary policy than more easing measures (from his note to clients yesterday):

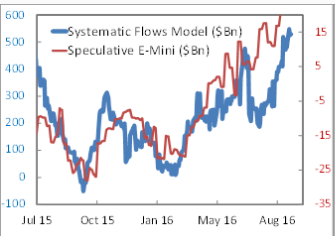

With upcoming ECB, BOJ and Fed meetings, investors are assessing the probability and potential impact of central banks taking steps towards the normalization of monetary policy. The impact of such a move would be negative for a broad range of financial assets, the same way as accommodative policy was positive in recent years. To prove that, we tested the link between the change in the total size of central bank balance sheets (Fed, ECB, BOJ, and BOE) and monthly returns of various assets. From the table below, one can see that CBs balance sheet has been a major driver of bond and equity prices globally (t-stat greater than 2 indicates a significant relationship, and we are finding t-stats of 3-6; Figure below left).

Most investors intuitively understand the concept of ‘a rising tide that lifts all boats’.

Just this morning, headlines from the ECB are less dovish then the market wanted. And with that we have seen an uptick in equity Volatility, via Bloomberg:

*ECB LEAVES MAIN REFINANCING RATE UNCHANGED AT 0%

*DRAGHI SAYS NO NEED FOR EXTRA STIMULUS ‘FOR THE TIME BEING’

*DRAGHI SAYS ECB DIDN’T DISCUSS EXTENSION OF ASSET-PURCHASE PLAN

The EuroStoxx 50 (SX5E) is down 1% on these headlines:

In light of Marko’s commentary, and the news this am, I’ll just reprint some of my commentary about the relative cheapness of short dated SPY options in the event of any surprises from the Fed (from yesterday’s morning note, (High (Low) Times):

We are kind of back to the 2015 playback with crowding into a handful of sectors, some antithetical to growth, and a few dozen stocks whose current growth (for now) justify lofty valuations. I think it is important to note that in 2015/early 2016 I found this set up in U.S. stocks troubling. On a couple occasions I was right, when too many investors headed for the door at the same time, the dislocations were massive with two very sharp draw-downs, but the subsequent V reversals, which have ultimately led to new highs and now a period of historic calm in the SPX have ultimately proven most market views wrong.

If the Fed were to surprise in two weeks, Sept 23rd weekly options in the SPY (the etf that tracks the SPX) are cheap in volatility terms, with 30 day at the money implied volatility at 9.25% (blue below), despite realized volatility (white below) being at all time lows at 5%:

From Bloomberg

This is an example where the options market has a difficult time in pricing in the unlikely (tail risk). The Fed funds futures have a 20% chance of a move in September. Without knowing exactly what a market reaction to that low probability event would be, rather than try to price in that 20% chance of the unknown, the options market merely ignores it.

But that can be good for hedging and directional bets. The SPY at the money straddle, expiring Sept 23rd is pricing in just a 1.8% move between now and then. That includes the Fed meeting and means the historically cheap volatility from a historically slow August is still available. It probably won’t last.

Following historically low vol to end the Summer, a stock market at all time highs and with the possibility of at least one vol shock in the market between now and year end, the options market is providing an opportunity for cheap protection. We’ll detail some ideas for portfolio hedges later today.