| Basic Terminology | Options | Volatility | Greeks |

Long/Short Stock Strategies | Calendar Spreads | Straddles and Strangles | Vertical Spreads | Butterflies |

| Straddle |

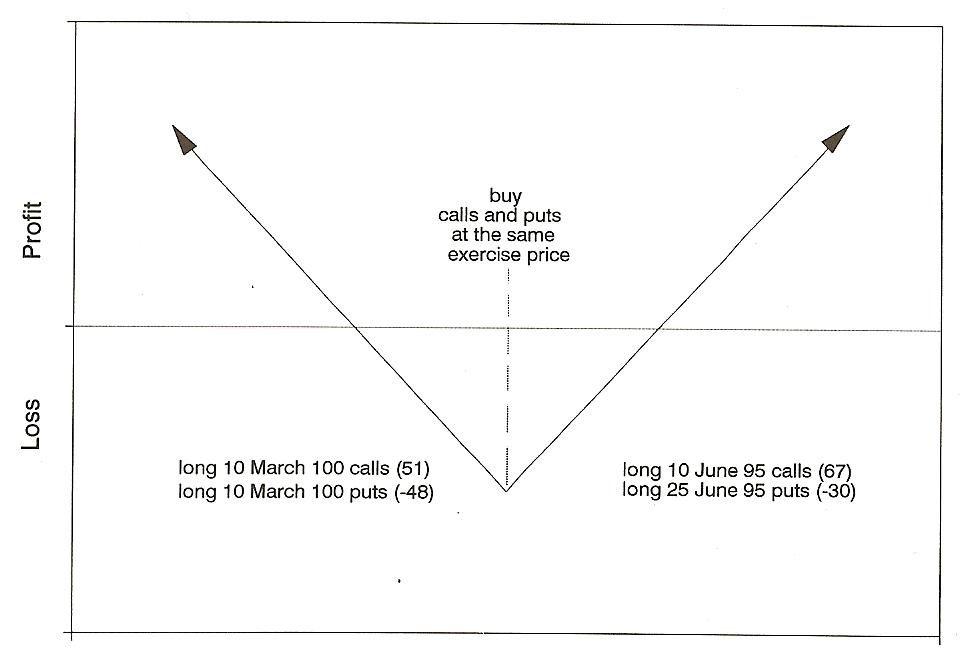

| Long Straddle |

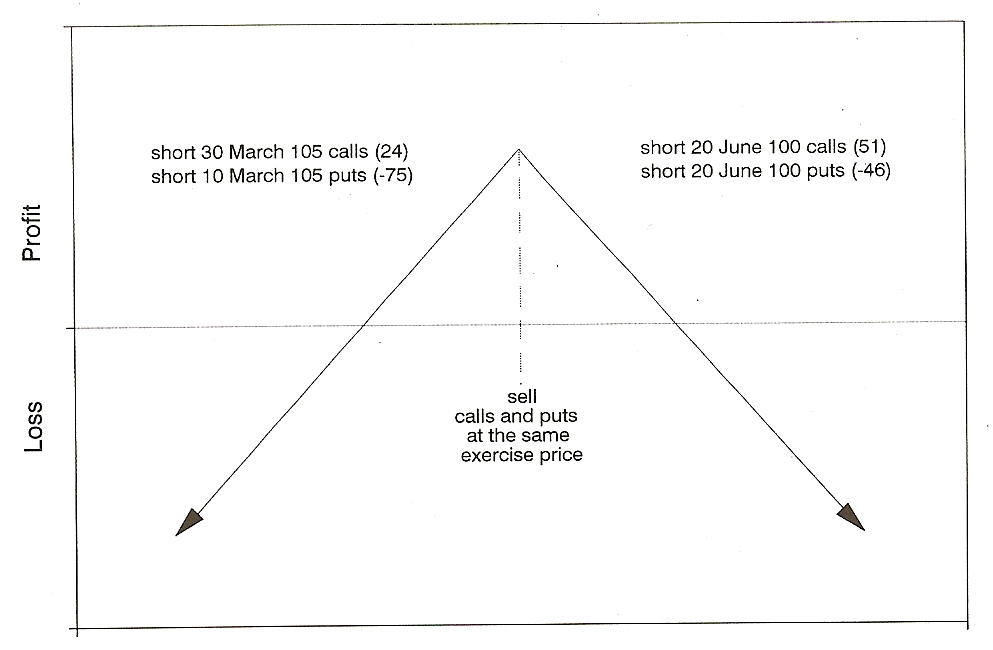

| Short Straddle |

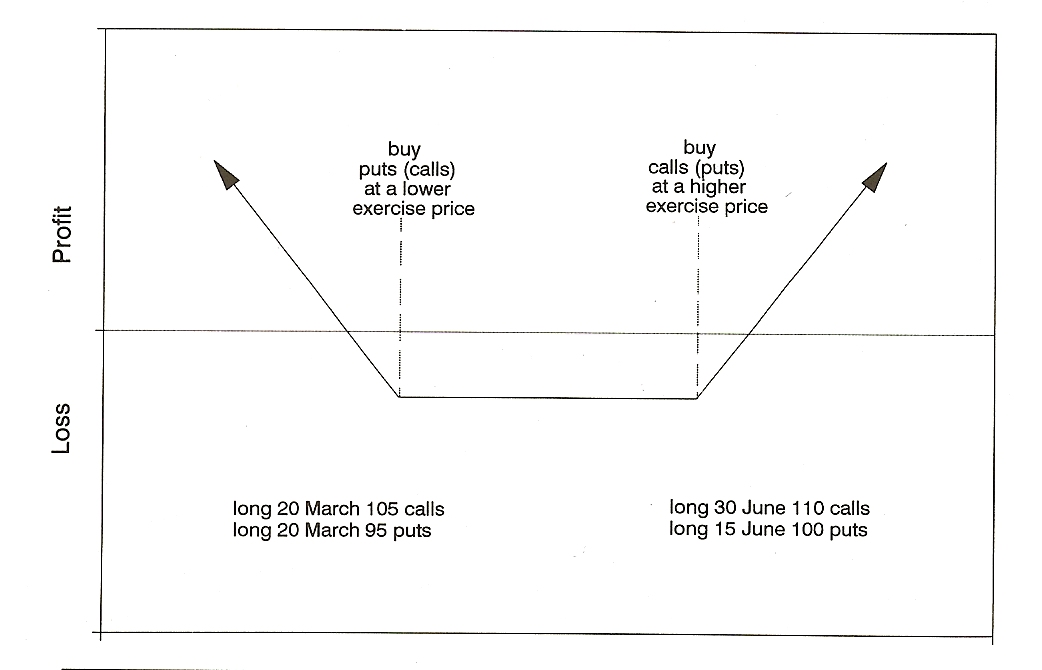

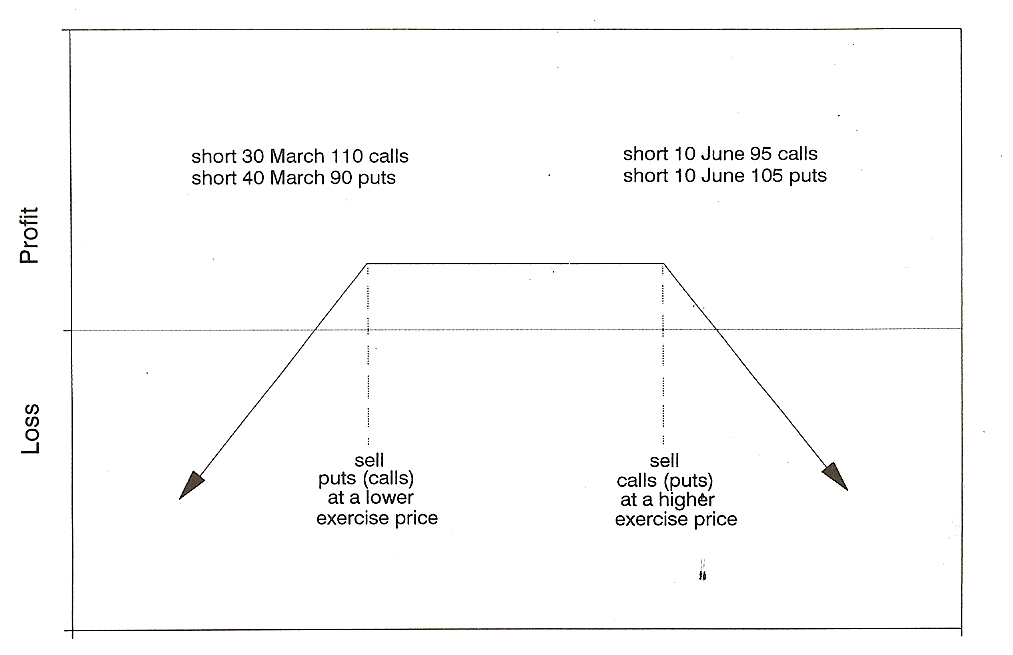

| Strangle |

Straddles and strangles are volatility strategies. They seem like simple strategies, but are in fact fairly advanced as your predictions must be quite accurate for them to work out.

A straddle consists of buying or selling both a call and a put of the same strike. Usually this is done with at-the-money options and therefor is initially a delta neutral strategy as at-the-money calls and puts have around 50 deltas, positive and negative, respectively. For a long straddle you buy the call and put and a short straddle you sell them.

Graphs of long and short straddle from Sheldon Natenberg, Option Volatility & Pricing, pps. 141, 142.

With a long straddle you are long gamma, long vega, and negative theta. By buying both the call and the put, you are spending money, buying premium. You need stock to move significantly in either direction and/or implied volatility to go up, all before too much time passes. Your upside and downside profit potential are unlimited (until stock reaches zero) and your maximum loss is what you paid for the straddle.

If you have bought a straddle near expiration, the time decay on the premium of the options will be extreme. Therefore, you will need stock to move either up or down beyond the price of the straddle to make money. A move up in implied volatility may or may not be enough to make up for the time decay. You might buy a near term straddle before an event if you think the move in the stock, up or down, will be greater than the price of the straddle. With this strategy it is important to look at historical moves after events. For example if it is an earnings, you might look at the previous three or more earnings to see if the stock has moved beyond the price of the straddle following the announcement. Many times the average earnings move is priced already into the options. That’s why this strategy takes some conviction and precision in what you are expecting. You also generally would want to sell the straddle quickly after the event as implied volatility will generally come in.

If you think stock will be moving around a lot over the duration of the life of the straddle you might buy with the expectation of scalping stock. As stock goes up the straddle will become a long delta position (the call goes in-the-money, the put out-of-the-money) and you can sell stock to stay delta neutral. As the underlying moves down you become short deltas (the put goes in-the-money and the call out-of-the -money) and you would buy stock to be delta neutral. With moves up and down you’d be scalping stock for a profit.

A long straddle further out will have less negative theta (time decay) and more positive vega. One might buy a long straddle a few months out if you think that volatility is trading especially low and that there could be stock movement or uncertainty occurring down the road that would cause implied volatility to go up.

Let’s say you are considering a straddle three months out. To make a volatility determination, you might look at 90-day historical volatility. Another consideration might be a year long graph of 30-day implied volatility. If 30-day implied volatility has not been below say 40 all year and you are buying lower than that then you might consider it low. You might look at where earnings and events fall in relation to the straddle and what implied volatility has done historically in relation to earnings and events. You might consider the volatility of the underlying versus other similar underlyings or the market as a whole.

You can see that even though a long straddle would seem to be a low risk strategy that it in fact requires a lot of consideration and precision of expectation in order to be profitable.

A short straddle, on the other hand, is a high risk position. As you can see from the graph that losses are unlimited and profits max at the price received for the sale of the straddle. Profits are only in the span of up or down the price of the straddle from the strike.

With a short straddle you are short gamma, short vega and positive theta. You want stock to stay still, implied volatility to come in and the option premium to just decay away. You might sell a straddle if you think that implied volatility is exaggerated compared to the movement you expect in the stock. In general, on the site, we won’t be exploring trades that involve naked short straddles, but might consider in a situation where a trader already has a stock position or where we do a short straddle as one part of a multi-tier strategy as Dan did going into PCLN earnings in February 2012.

Strangles have many of the same characteristics as straddles, but with a larger margin of error. For a strangle you buy or sell both an out-of-the-money call and an out-of-the-money put of the same expiration. Thus the premium paid or received is considerably lower than a straddle. On the other hand, with a long strangle you need the stock to move quite a bit farther or volatility to go up quite a bit more (vega being smaller out-of-the-money) for it to be profitable. A short strangle has a larger area of profitability, but the maximum profit is not as great because the premium received for out-of-the-money options is less. The theta is also smaller so decay will not be as dramatic.

Graphs of long and short strangle from Sheldon Natenberg, Option Volatility & Pricing, pps. 143, 144.

You might put on a long strangle if you think there is a chance stock might make a big move, but your conviction isn’t high enough to pay the premium for a straddle. Or as in the PCLN example given above (this link is to analysis) as a hedge to a riskier strategy to take advantage of a volatility skew between months.

Strangles tend to be a lower premium strategy as compared to straddles, but the probability that you lose all of your premium is also higher. If you think volatility is low, you can buy a straddle that has a higher probability of being profitable if you are correct, but the strangle has a much higher payout if the stock makes an extreme move. Your decision will depend on your expectations, your risk tolerance and your conviction.

Both straddles and strangles are strategies to take advantage of a perceived mispricing of options where the trader thinks that implied volatility or premium does not represent what the underlying will do, but where he or she does not have a strong directional opinion. They are often tempting, but should definitely be used with consideration. The risks of short straddles and strangles are obvious, but a slow death by decay can be extremely tortuous as well.