For the better part of the last 6 months, investors have been fairly clueless as to where to park cash with the prospects of a reasonable risk adjusted return. The global volatility in credit, currencies, commodities and emerging market equities that was prevalent for the latter part of 2014 and the first half of 2015 hit our shores in a major way late last summer, and its been my view that at the moment (really for weeks/months leading up to the flash-crash of August 24th), the risk reward of placing blind faith in the Fed to keep U.S. equities values bid changed for the worse in a very big way. The ingredients that made the QE/ZIRP induced bull market in stocks so irresistible to investors seemed to be coming to an end with the Fed’s increasingly hawkish tone juxtaposed with the increasingly dovish tone by the BOJ, ECB and PBOC. And then wham, the U.S. Fed ripped off the ZIRP bandaid in mid December, and all high holy hell broke loose in global risk assets. I know, I know, we are down less than 5% on the year, and less than 10% from the S&P 500’s all time highs, so in many ways the recent volatility might have served a fairly decent purpose by shaking out some weak hands, doing away with excess risk takers.

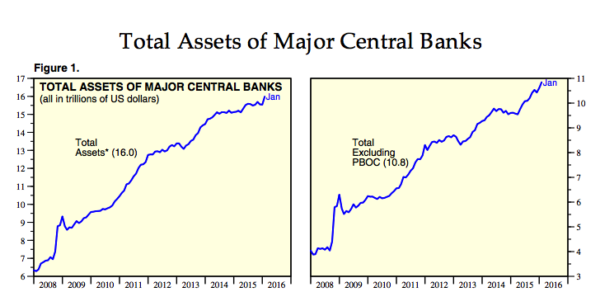

That’s all fine and good, but let’s not forget the recent commentary by Fed officials, and maybe more importantly c-level execs of fortune 100 companies who’ve acknowledged the potential for capital markets volatility to restrain growth the world over, growth that has been amazingly hard to stimulate, despite overly accommodative monetary policy which has included the expansion of global central bank balance sheets by more than $10 trillion since the financial crisis, from Ed Yardeni Research Feb 12th:

So now we live in a world where Central Banks need to get a tad more creative than merely buying stocks and bonds, and find themselves adopting a new interest rate policy, that of negative rates for deposits that flies in the face of all logical premises of modern finance. Trust me, I am not smart enough on such topics to have any clue how this is all gonna shake out, but I kind of feel it in my plumbs that in the intermediate term it’s gonna end very badly for risk assets like stocks. As we head into March with investors far more sanguine about risk taking than they were just a few weeks ago, its important to consider that the message and actions from the BOJ, ECB & the FOMC, who all meet in the next three weeks, is not likely going to be one of strength or confidence in the global economy. The waning global equity rally over the last year is in my opinion reflective of investors waning faith in central banks, or merely a vote of the future effectiveness of existing monetary policy. That is not a particularly original thought, but I just don’t get how investors can totally disregard a piece of data (yes it’s just one piece of data) like Markit’s Services PMI print for February that showed the first contraction in services here in the U.S. in 27 months:

Markit’s #PMI shows significant risk of US economy falling into contraction. Full analysis: https://t.co/usD7YYrXsCpic.twitter.com/pjijgDOtzq

— Markit Economics (@MarkitEconomics) February 24, 2016

There has been a lot of talk about the probability of a recession. I think there are a lot of smart people wasting a lot of time trying to figure out the likelihood of an economic event that will only truly be known after the fact. What seems fairly obvious to me is that the risk taking mood has changed, at a time where global growth feels closer to contracting than accelerating and central bank policies seem at their least effective and most extreme positioning since the start of the financial crisis in 2007. I do not see this as a good time to be dipping your toe in U.S. stocks if you have an intermediate term time horizon, even if you think (as I do) that the SPX could keep running to possibly 2050. The higher we go in the near term the greater the chance for a violent move lower in my opinion, and its been my view that the next test of 1800ish in the SPX on the downside could likely yield a fairly violent break to 1600ish. I’ll leave you with a tweet from one of my favorite follows on Twitter, @NorthmanTrader that I saw this week, which more than adequately sums up my view of investor sentiment and the current trade set up in U.S. stocks:

If you were too scared to buy in the low 1800s but are now chasing into 1940s you are trading backwards.

— Northy (@NorthmanTrader) February 18, 2016

As for my positioning: [private]

Into the Feb 11th lows we covered a lot of shorts (see here) and the week after did a fairly good job of sitting on our hands acknowledging the potential for a sharp bounce. Last week and early this week we got a bit more aggressive in shorting sectors (always with defined risk, that’s just what we do at RiskReversal) that we thought ran to far too fast with no fundamental improvement (XRT, XLB & QQQ), and now we will have to manage that defined risk by cutting our losses. That’s the way it goes in trading.

[/private]